Why We Sell Winners and Marry Losers

The mistake we all make — even when we see it coming

There’s a card in my vault I’ve held for years for one reason only: so I don’t have to admit a loss. The market isn’t moving. No catalyst. I know I should sell — and I keep putting it off. Meanwhile, a card I sold three years too early is now worth twenty times what I got for it. This isn’t a story about two cards. It’s a story about one mistake we all make — and about why we make it even when we see it.

It’s a flaw in how the mind works — mine, yours, everyone’s who has ever held a position and watched it rise or fall. The flaw has a name: the disposition effect. And today you won’t get another story — you’ll get the mechanism from the inside. Why you have it too, even if you think you don’t.

What it is

The term comes from 1985, from a paper by Hersh Shefrin and Meir Statman. Its title is the whole thesis: “The Disposition to Sell Winners Too Early and Ride Losers Too Long.”

It has two sides — and they’re exact opposites. You sell winners too early — you lock in a sure gain before it ripens. And you hold losing positions too long — you refuse to close one and wait for it to “come back.” It isn’t about mood. It isn’t greed one day and fear the next. It’s a systematic asymmetry that always pulls the same way.

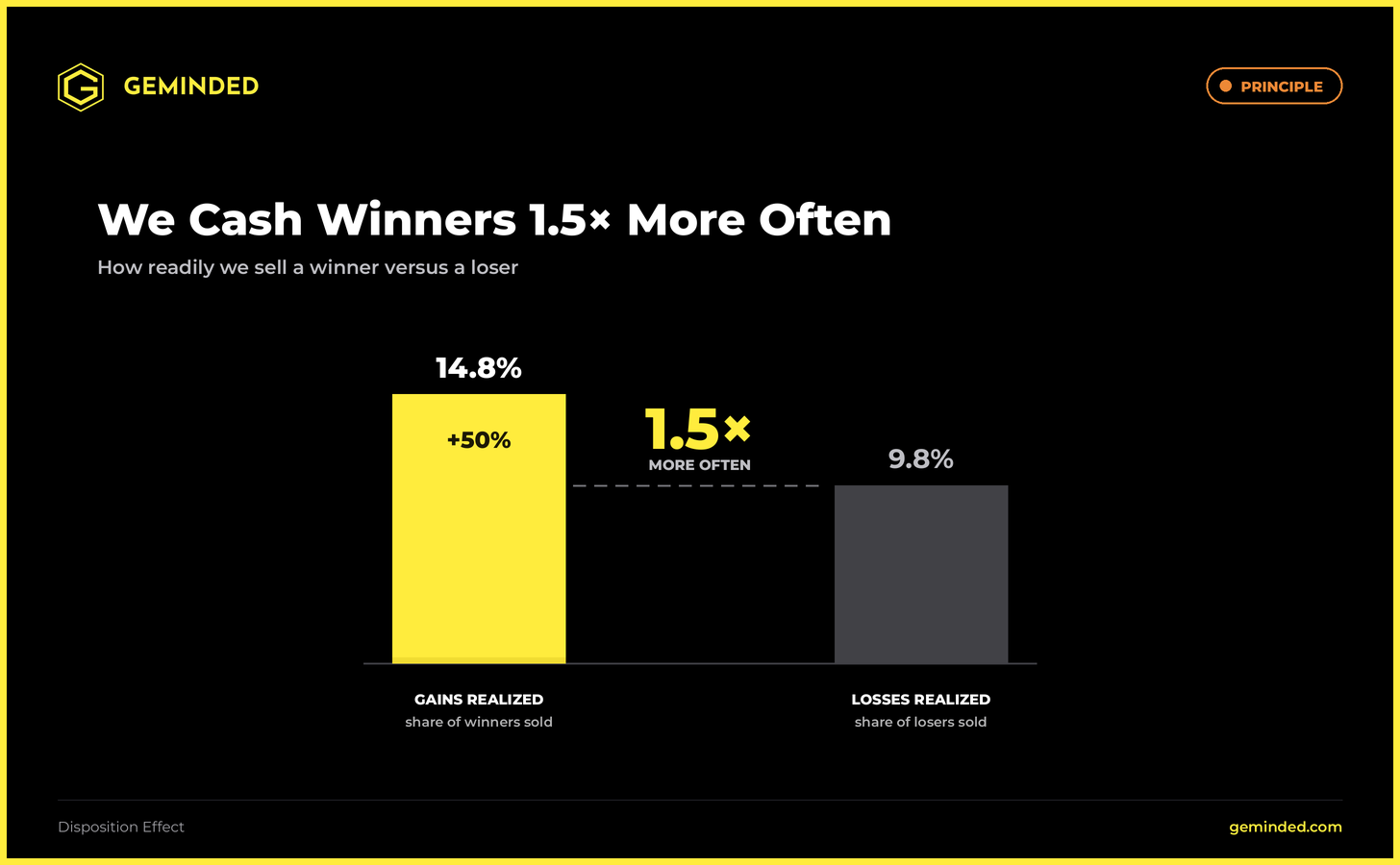

And this isn’t soft speculation. In 1998, Terrance Odean went through the trading records of 10,000 real brokerage accounts. The result: investors realized gains 1.5× more often than losses — 14.8% of gains booked versus 9.8% of losses.

Now, here’s the first objection waiting to be raised: doesn’t that just mean they invested well and had more winners? No. The number doesn’t measure how many winners they had — it measures how they treated them. Out of all their winning positions, they sold a far larger share than they did of their losing ones. When they were up, they took the gain. When they were down, they held and waited. Same decision environment, opposite behavior. “They invested well” doesn’t explain that.

No survey, no lab. Real trades by real people with real money. The effect shows up across the US, Europe and Asia, among retail and institutional investors alike. It’s one of the most robust facts we have about how investors behave.

Why it happens

Shefrin and Statman saw four psychological forces behind it. Don’t read them as a list — read them as four forces pulling the same way, each of which I know from my own head.

Loss aversion — the engine. Kahneman and Tversky showed that a loss hurts roughly twice as much as an equal gain feels good. It’s not an impression — it’s an asymmetry built into how we value things (a coefficient around 2.25). What that means for your decisions: realizing a gain is a small, certain pleasure now. Realizing a loss is a large, certain pain now. The brain instinctively takes the pleasure and defers the pain.

Mental accounting — the ledger in your head. You run every card as a separate account against the price you paid for it. Until you sell, the account is “open” — the loss is only on paper, it can still “come back.” The moment you sell, you close the account and the paper loss turns into a final, booked defeat. Which gives one of the most important sentences in this whole piece: your purchase price is psychologically sticky but economically irrelevant. The market doesn’t care what you paid. Price is set by what the card can actually fetch today based on recent sales — not by your account.

Regret avoidance — dodging the admission of a mistake. Selling at a loss means actively admitting: I was wrong. Holding means postponing that admission. Selling a winner, by contrast, brings pride — “I was right, I cashed in.” The mind collects pride and runs from admitting it was wrong, even when that costs it money.

Self-control — willpower versus desire. Shefrin has his own apt term for it: get-evenitis. The urge to at least break even, to get square, to “not lose on it” — before I close the position. It’s the disease of breaking even. And we all know it.

Four different forces, one direction: hold what’s falling, sell what’s rising. Exactly the opposite of what the math would want.

Why it hurts more with cards

This is where most articles on the disposition effect stop — at stocks. And where the part that interests me about cards begins. Because the effect isn’t tied to the stock market. It’s documented on markets that trade slowly, and where you have a relationship with the asset.

In 2001, David Genesove and Christopher Mayer studied the Boston condo market. Owners sitting on a nominal loss set noticeably higher asking prices than those sitting on a gain — they passed part of their loss straight into the price and waited months for a buyer who often never came. Loss aversion isn’t a stock-market anomaly. It lives anywhere the asset is illiquid and emotionally charged. And a card is both — more so than a stock.

Three reasons a card hands your head more excuses than a stock does:

No daily price. A stock is priced every second. A card isn’t. A “paper loss” is far easier to keep calling “temporary” when no one is repricing it out loud every day.

Emotional ownership. You don’t hold a stock in your hand. A card you do. The collector’s attachment amplifies mental accounting — the reference point (your purchase price) gets even stickier when a piece of you is attached to it.

Illiquidity masks the mistake. When a card barely trades, “it’s just not selling yet, I’ll wait for the right buyer” sounds reasonable. And sometimes it’s true. Other times it’s just get-evenitis dressed up as patience. And from the outside, the two look exactly alike.

The card market hands your head every excuse the stock market doesn’t.

And there’s one more layer. With scarce and ultra-rare cards, many lean on CardLadder Value as an “objective” number. But it’s precisely the rarest pieces the index often underprices. It doesn’t apply across the board — but when it happens, even the reference point you’re basing your decision on sits below reality. And that only feeds the disposition effect: “hold” is whispered to you by both the bias and an underpriced index.

Two examples from my portfolio

Theory is nice. Now two cards from my investment collection — each showing one half of the bias. And with one of them I’ll tell you straight: I don’t know which side of the line I’m on.

A winner sold too early — Kaboom. This is Exhibit A, and you already know it from the last article, so briefly. A 2018 Panini Kaboom Messi Gold, one of ten copies, PSA 10. I bought it brilliantly, sold it in 2022 into the post-covid slump at a profit — but far below what it’s probably worth today. I took a sure gain now. It cost me all the growth that came after. A textbook disposition effect.

You can’t buy the same card back — and if you could, certainly not for what you sold it for.

A held losing position — or a thesis? A 2016-17 Donruss Optic Giannis Black 1/1, BGS 9.5. I bought it during covid, fairly expensive. Today its price is highly uncertain — by current CardLadder Value roughly a third of what I paid, and CL Value tends to run conservative on cards this rare. I’ve held it for four years, still hoping it climbs.

Notice that word: hoping. That’s exactly the language get-evenitis speaks. “It still has potential, I’m just waiting for the right moment.” That’s how everyone sounds who’s holding a loss and won’t admit it. A bias never presents itself as a bias — it always dresses up as a thesis.

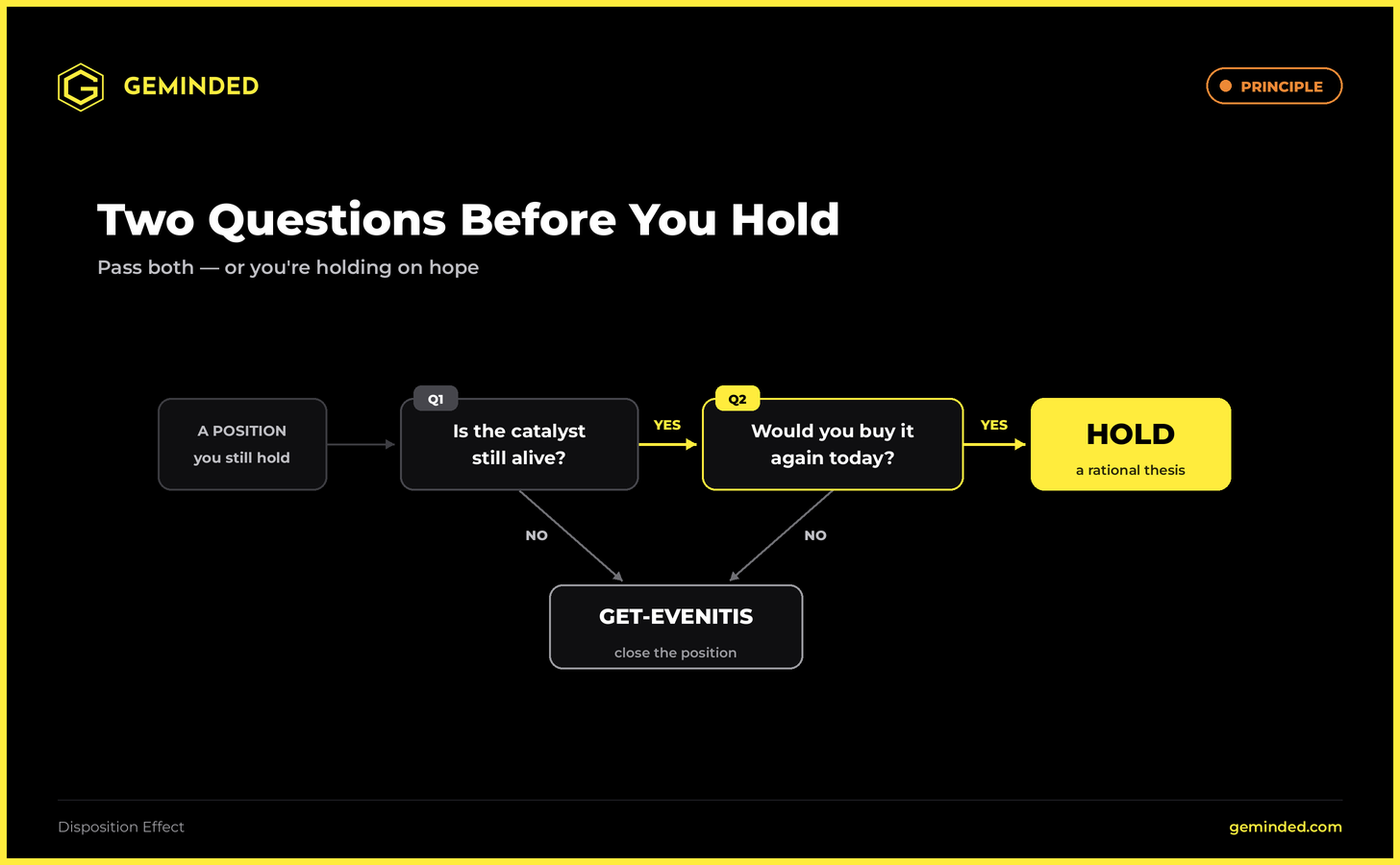

So I asked myself a question I’ll put to you in a moment: if I didn’t own Giannis today and had the same cash — would I buy him at the current price as a fresh position? For Giannis, my answer is yes. And why, the next section settles.

When holding a loss is NOT a mistake

Now the most important distinction in this whole article — otherwise it collapses into the naive advice “always sell whatever’s in the red.” That would be wrong. The disposition effect is about the REASON, not the action. Holding a losing position can be perfectly rational. It depends on why.

The thesis hasn’t changed, only the price. When the fundamentals still hold and only the current price has dropped, holding is right — that’s not bias, that’s patience. For rare, irreplaceable positions it’s doubly true.

Illiquidity as a fact, not an excuse. For genuinely rare cards, “wait for the right buyer” is a real approach. But only when you can separate it from rationalization. The test is simple: would you sell it today at fair value if someone offered it? If yes, you’re holding for the future, not for the purchase price — and that’s fine. If it bothers you to sell “below what you paid,” you’re holding because of get-evenitis.

Taxes. Odean saw this in the data too: in December the ratio flips — people suddenly realize more losses than gains, because tax optimization overrides the bias. Realizing a loss can make legitimate tax sense. Sometimes selling at a loss is the smarter move, not a capitulation.

And here I come back to Giannis. My answer “I’d buy him again” wasn’t a defense — it was a test, and Giannis passed it. I hold him because the thesis is alive: he’s deeply undervalued against the market, he’s an active player with a clear catalyst (he wants out of the Bucks, and where he lands is the open question), and he’s still a 1/1. That isn’t get-evenitis. That’s a thesis with a defined decision point.

The hard part isn’t knowing the rule. The hard part is telling a good reason from a good excuse.

What to do about it — my antidote

Most articles write “set your rules in advance and stick to them” here. True, but empty. Here’s what I actually do — and it isn’t a slogan, it’s a decision framework I run every position through.

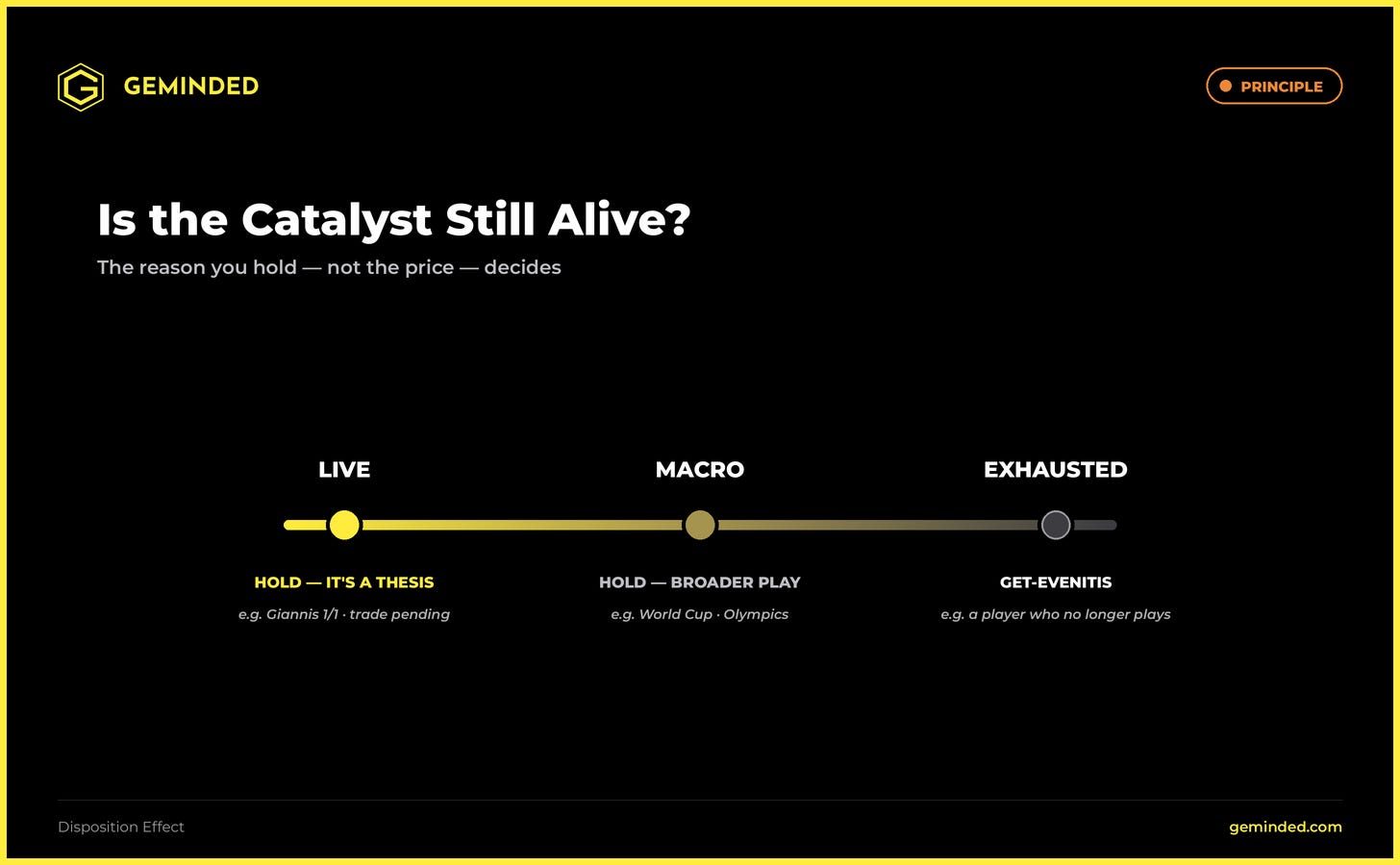

The purchase price doesn’t decide. The catalyst does. Instead of asking “what did I pay?” I ask “what moves this card next?” And I sort catalysts into three types:

A live catalyst. An active player, a near and concrete event that can move the value (a trade, a title, an MVP season). Giannis 1/1: waiting on his destination after the Bucks. Holding makes sense because the decision point is close and binary.

An exhausted catalyst. No clear future trigger. The card holds its price but goes nowhere. This is where get-evenitis attacks hardest — and where a hard rule has to step in. I hold a card in my portfolio of a player who no longer plays and whose market hasn’t moved in years: direct comps are still the same, the last time a card identical in grade sold, a few months ago, it went for the same money as before. No catalyst. Inside, I want it to climb at least a few thousand — but that’s get-evenitis now, not analysis. So I have a clear rule for this card: I won’t wait forever. Soon I’ll send it to auction and close the position.

A macro catalyst. A big event that lifts not a single player but a whole segment — a World Cup, an Olympics. A different logic than for an individual; we’ll save that one for another time.

And here’s the hardest part, not the technical one: the loss has to be accepted, written into a cell in Excel — because until it’s written down, it isn’t real. This one will have to be. Capital frozen in a stagnant losing position isn’t working; even the smallest proceeds I move elsewhere, where there is a catalyst.

I mention that exhausted position here only as an example of the mechanism. It has its own story — far deeper, a different market, a direct comparison with Kaboom, and the question of why the market values some careers higher than others even when the numbers say otherwise. Several factors play into it — and one of them is how a player is remembered. That one gets its own article.

Which card in your collection is an “open account” you refuse to close — and is it a thesis, or get-evenitis?

Write to me; I read every reply.

Next time: how big events — the World Cup, a week away — move card prices. FOMO, the other side of this coin, will have to wait. Which, for a piece about the fear of missing out, is actually pretty funny.

— Geminded